Madison Eubanks

Madison Eubanks

How Advisors Can Initiate Estate Planning Conversations—And Why They Should

For wealth management firms that want to offer their clients complete, holistic financial advice, estate planning services are an absolute must. The snag is that most firms have far more advisors than planners, and resources don’t allow central planning teams to work closely with every single client.

Because estate planning is an important part of the client experience, planners need to find ways to scale the practice to the advisor level. This doesn’t mean advisors need to become the final authority on all things related to estate planning, but rather that they need to know enough to open the door to estate planning conversations with clients.

Before we get into how advisors can begin having these conversations, let’s look at some reasons why advisors should be talking about estate planning with their clients.

If you prefer to dive right in, download The Planner’s Guide to Scaling Estate Planning to Every Client here.

The benefits of advisor-led estate planning conversations

Estate planning is an intimate topic. It might involve discussing complicated family dynamics, assessing beneficiaries’ needs and ability to handle finances, thinking through uncomfortable what-ifs like a divorce or an unexpected death, and more.

These can be difficult subjects, but these conversations can lead to a far stronger client/advisor relationship than financial planning alone. By building that trust, advisors are more likely to retain clients, engage their families and beneficiaries, and ultimately grow their firm’s business.

Additionally, the benefits of offering estate planning can include:

- Tailored recommendations and services enable a firm to engage more clients and extend additional in-house offerings. Clients will appreciate being able to accomplish more financial planning in one place, rather than bouncing around between firms for different services.

- Offering specialized services and niche advising skills can establish a firm’s reputation for estate planning—making it able to attract wealthy clients who have complex estates.

- Engaging clients proactively and connecting with multiple generations can drive long-term client retention.

- Advisors who are involved in a client’s estate planning process are able to see the entire balance sheet, which can lead to all-around better financial planning and advice.

Practical advice for initiating estate planning conversations

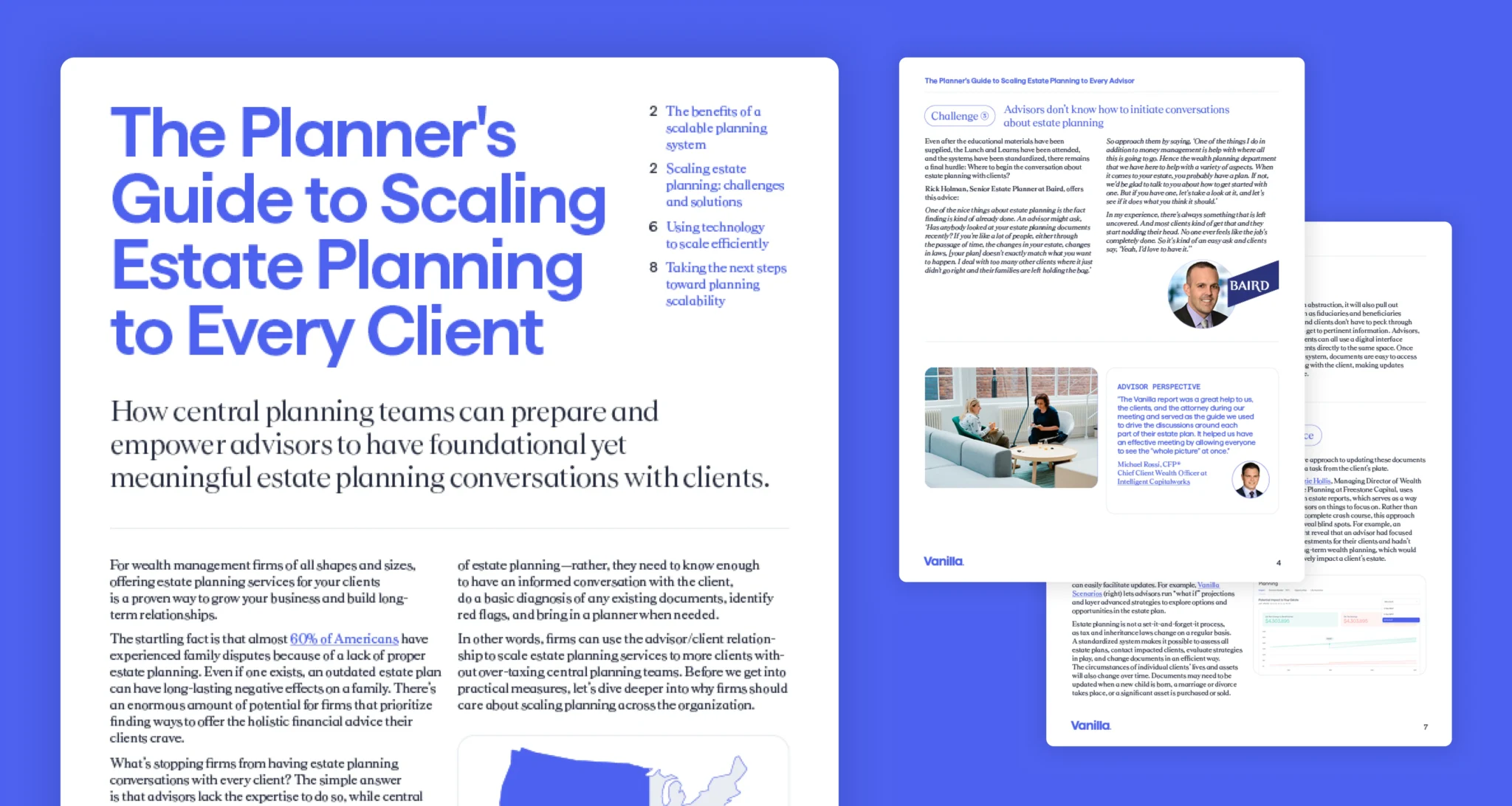

Even after the educational materials have been supplied, the Lunch and Learns have been attended, and the systems have been standardized, there remains a final hurdle: Where to begin the conversation about estate planning with clients?

Rick Holman, Senior Estate Planner at Baird, offers this advice:

One of the nice things about estate planning is the fact finding is kind of already done. An advisor might ask, ‘Has anybody looked at your estate planning documents recently? If you’re like a lot of people, either through the passage of time, the changes in your estate, changes in laws, [your plan] doesn’t exactly match what you want to happen. I deal with too many other clients where it just didn’t go right and their families are left holding the bag.’

So approach them by saying, ‘One of the things I do in addition to money management is help with where all this is going to go. Hence the wealth planning department that we have here to help with a variety of aspects. When it comes to your estate, you probably have a plan. If not, we’d be glad to talk to you about how to get started with one. But if you have one, let’s take a look at it, and let’s see if it does what you think it should.’

In my experience, there’s always something that is left uncovered. And most clients kind of get that and they start nodding their head. No one ever feels like the job’s completely done. So it’s kind of an easy ask and clients say, ‘Yeah, I’d love to have it.’’

Keeping the estate planning conversation going

Estate plans — especially those for UHNW clients — must be kept up to date with changes in life and law. Typically, existing plans are reviewed by an attorney at the client’s request, but specialized software like Vanilla can make this process much easier to execute on a regular basis. Additionally, a strategy that made sense for a client’s financial situation when they created their original plan may not suit their current circumstances, and therefore need reassessment.

Running an analysis can be done faster because specialized software creates a system that keeps up-to-date information on each advisor, their clients, and the documents kept on file. Once they have identified clients with missing or incomplete plans, the advisor can easily facilitate updates. For example, Vanilla Scenarios lets advisors run “what if” projections and layer advanced strategies to explore options and opportunities in the estate plan.

Estate planning is not a set-it-and-forget-it process, as tax and inheritance laws change on a regular basis. A standardized system makes it possible to assess all estate plans, contact impacted clients, evaluate strategies in play, and change documents in an efficient way. The circumstances of individual clients’ lives and assets will also change over time. Documents may need to be updated when a new child is born, a marriage or divorce takes place, or a significant asset is purchased or sold. Taking a proactive approach to updating these documents means removing a task from the client’s plate.

For example, Vanilla’s platform enables Dogwood Wealth Management to have annual estate planning conversations with each client in their book of business. Dogwood’s focus on holistic financial and estate planning underpinned by technology allows the firm to work efficiently and helps drive continued growth and client satisfaction.

For more insights on how to scale estate planning to more advisors at your firm, download the complete guide.

Published: Jun 05, 2024

Holistic wealth management starts here

Join thousands of advisors who use Vanilla to transform their service offering and accelerate revenue growth.