Jessica Lantz

Jessica Lantz

From postscript to plan: Why charitable trusts are moving to the center of the estate conversation

Estate planning conversations don’t always start with a trust structure. Sometimes they start with a client who wants to give — to a cause they care about or to an institution that shaped who they are. What makes these conversations worth having carefully is that charitable intent and estate planning goals don’t have to live in separate lanes. When structured thoughtfully, a charitable strategy can honor a client’s values while doing meaningful work on their estate at the same time.

That integration is increasingly where advisors are finding differentiation. Clients with appreciated assets, concentrated positions, or taxable estates are asking harder questions — not just “how do I give?” but “how do I give in a way that also makes sense for what I’m leaving behind?” The advisors best positioned to answer those questions are the ones who can model the options and show the impact.

The charitable planning toolkit

Philanthropic clients often arrive at this conversation with very different goals. Here’s a look at some of the most commonly used strategies — how each one works, and which client situations each fits best.

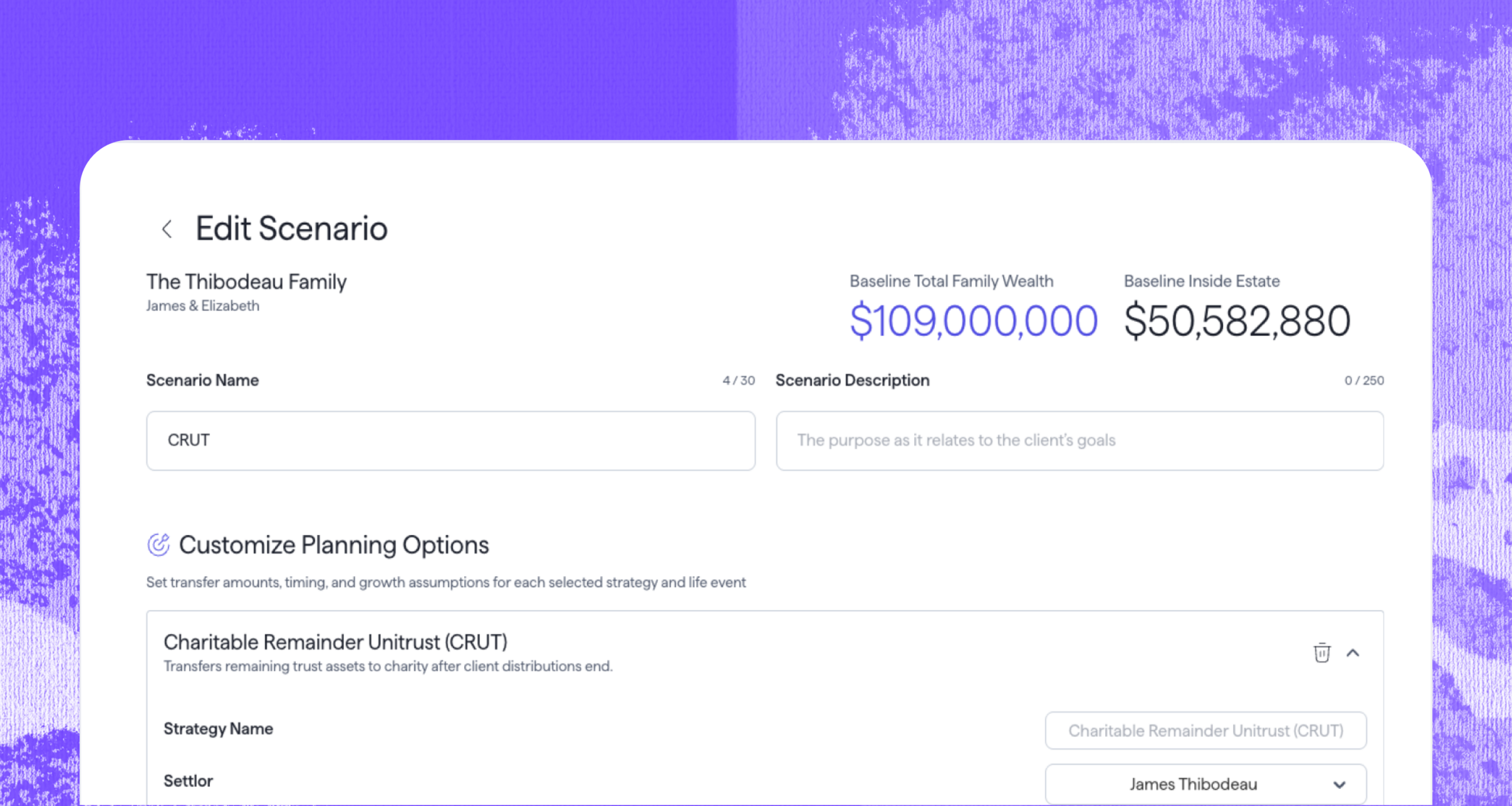

Charitable Remainder Unitrusts (CRUTs) are a strong fit for clients holding concentrated, low-basis assets who want to diversify without triggering an immediate capital gains bill while generating an income stream. The trust pays a fixed percentage of its assets — revalued each year — to a non-charitable income beneficiary for life or a term of years. Whatever remains at the end passes to charity. In Vanilla Scenarios®, you can configure the income beneficiary, payout rate, and term, with automatic enforcement of the IRS 10% remainder requirement. An existing or new Donor Advised Fund (DAF), Private Foundation, or other charitable organization can be designated as the charitable remainder beneficiary directly within the scenario.

Charitable Lead Annuity Trusts (CLATs) run in the opposite direction. The trust pays a fixed annuity to charity for a term of years, with the remainder passing to heirs at the end — making them particularly effective for clients who want to benefit charity now and pass remaining wealth to the next generation tax-efficiently. In lower interest rate environments, a well-structured CLAT can transfer significant wealth with minimal gift and estate tax impact, because the hurdle rate set by the §7520 rate is easier to outpace.Vanilla models these as zeroed-out grantor CLATs, with controls for the charitable term, §7520 rate, and growth rate.

For clients where a trust structure isn’t the right fit — or where ongoing giving is already part of the picture — outright gifts to charity are worth keeping in the conversation. A direct transfer of cash or appreciated assets reduces the taxable estate, and for clients who give through a DAF, the DAF can be selected as the charitable recipient within the scenario in Vanilla. This makes it straightforward to show the estate impact of a gift that the client will distribute to their chosen charities on their own timeline.

What the first wave of activity is showing us

Theory is one thing. Behavior is more interesting.

In the first 90 days since these tools went live in Vanilla Scenarios, 20% of all strategies included a charitable trust. More revealing than the headline number is how those scenarios were built. In nearly a quarter of them, advisors didn’t just enter a funding balance — they assigned specific asset accounts to the trust, modeling the actual holdings that would flow through. Modeling a charitable trust against a defined position is the difference between a hypothetical and a recommendation a client can act on.

Taken together, the signals point to advisors treating charitable trusts not as exotic add-ons but as structural choices on equal footing with the SLAT, GRAT, and IDGT work they’ve been doing for years. And for clients with both meaningful charitable intent and taxable estates, that shift in how advisors are thinking about these tools is worth paying attention to.

Putting it together

Charitable planning and estate tax efficiency are often treated as separate conversations. The advisors who are standing out are the ones who connect them — showing a client how a CRUT handles the low-basis position they’ve been carrying, or how a CLAT changes the projected estate picture twenty years out, or how a direct gift to their DAF today affects what their heirs receive tomorrow. These aren’t exotic strategies. They’re the right tools for clients who have both philanthropic intent and meaningful assets, and they’re worth bringing into more conversations.

A note for Washington state clients

Charitable strategies are one way to manage estate tax exposure. The underlying rules are another — and Washington just changed theirs effective July 1, 2026.

The two biggest changes your clients will notice: the exemption shifts to $3 million (inflation-adjusted annually starting in 2027), and the top marginal rate drops from 35% to 20% — a meaningful difference for larger estates. The new brackets range from 10% on the first $1 million of taxable estate up to 20% on amounts above $9 million. These new rules are already reflected in Vanilla projections today, with a full switch across the board on July 1.

A few things remain unchanged: there is still no portability between spouses of unused Washington estate tax exemption, the state QTIP election continues to be available, and the ratio approach for nonresident calculations stays the same. If any of your clients have Washington state exposure, this is a good moment to revisit their plans with the updated numbers in view.

Already a Vanilla customer? Reach out to our CSM team to explore charitable planning in Scenarios or to review how Washington state estate tax changes affect your clients. Exploring Vanilla for the first time? Request a demo.

Note that all unpublished features and enhancements mentioned are subject to change in both content and timeline without notice. Vanilla reserves the right to modify or cancel roadmap items at any time.

Published: May 27, 2026

Holistic wealth management starts here

Join thousands of advisors who use Vanilla to transform their service offering and accelerate revenue growth.