An Advisor’s Guide to Helping Clients Navigate Market Volatility

A 2026 analysis of more than 12,000 advisor-client meetings found that 72% of clients express interest in estate planning but defer. Only 26% move forward. Most clients aren’t opposed — they’re waiting for a reason to act now. Volatile markets provide one.

When markets are turbulent, it’s a smart time to revisit estate planning. While the instinct might be to pause and wait for stability, volatile periods can actually open up strategic opportunities.

Using the blog The Building Blocks of Estate Planning Techniques as a guide, we’ll outline some timely actions advisors can take to calmly and confidently help clients at different wealth stages navigate periods of uncertainty.

For a quick reference, download the complete cheat sheet for estate planning strategies to use by wealth stage here.

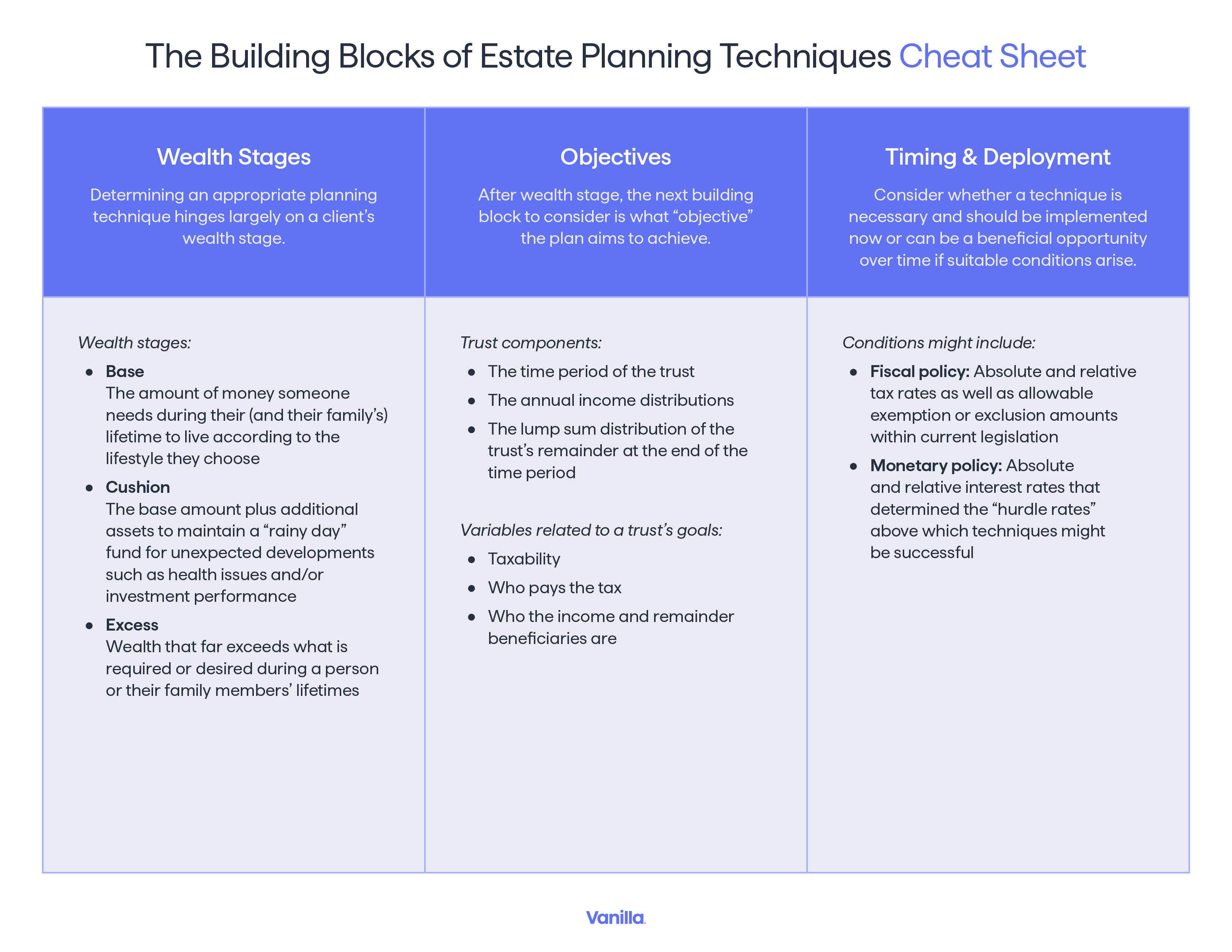

Base wealth stage: Financial planning foundations

Clients at the base wealth stage are focused on building and protecting what they have. In volatile markets, that means managing liquidity, taxes, and cash flow before thinking about transfer strategies.

Budgeting and liquidity

Market swings can expose cash flow vulnerabilities that were invisible in calmer conditions. Help clients map income against fixed and variable expenses, identify where stress points might emerge, and distinguish genuine needs from discretionary spending. Liquidity planning now prevents forced decisions later.

Roth IRA conversions

When markets sell off, account balances drop, and so does the tax cost of converting a traditional IRA to a Roth. A client who converts at temporarily depressed values pays taxes on a smaller balance, then benefits from tax-free growth as assets recover. The math is straightforward; the window is time-sensitive.

Tax loss harvesting

Volatility creates opportunities to sell positions at a loss and offset gains elsewhere in the portfolio. Systematic harvesting can meaningfully reduce a client’s income and capital gains tax burden without changing their long-term investment posture if positions are reinvested thoughtfully.

Cushion wealth stage: Estate planning

Clients with a cushion of wealth above their lifetime needs are approaching (or have crossed) the threshold where estate taxes become a real consideration. For them, volatile markets open up gifting and transfer strategies that work specifically because asset values are temporarily lower.

Leveraged gifting

When an estate sits near the taxable threshold, the key question is whether future asset growth happens inside or outside the current generation’s estate. Strategies like GRATs and IDGTs are funded with assets today and transfer future appreciation to heirs. They work best when asset values are depressed at the time of funding because the appreciation that happens afterward is what gets transferred tax-free. Volatile markets create exactly that setup.

Annual gift exemption

Clients can give up to $19,000 per beneficiary per year ($38,000 per couple) without touching their lifetime exemption. In uncertain markets, annual gifting is a low-friction way to systematically move assets out of an estate. It doesn’t require a market call, just consistency.

Wealth transfer as a planning anchor

For clients distracted by short-term volatility, estate planning offers a productive reframe. Conversations about asset allocation across legal structures such as trusts, entities, and gifting vehicles, shift attention from daily market noise to long-term family goals. That’s a conversation advisors are well-positioned to lead.

Excess wealth stage: Legacy planning

Clients in the excess wealth stage have more assets than they’ll need in their lifetimes. For them, volatile markets are a gifting opportunity: lower valuations mean more economic value can be transferred within the same exemption limits.

Gifting assets at lower valuations

A business or portfolio worth $20 million in a bull market might be valued at $15 million in a downturn. Using the same lifetime exemption during a downturn transfers 33% more economic value. The key is having enough conviction in the client’s overall financial position to move forward when prices are low, which is exactly where an advisor’s guidance matters.

Lifetime exemption

The current individual lifetime exemption is $15 million ($30 million per couple), now permanently extended. There’s flexibility in using it all at once or over time, and in choosing which assets to gift. Higher-cost-basis assets are generally better candidates. Lower-cost-basis assets held until death receive a step-up, which eliminates embedded gains. Help clients think through asset selection, not just the amount.

Multi-generational relationships

Estate planning naturally draws in the next generation. Advisors who are present for those conversations — helping families structure wealth transfers across generations — are far more likely to retain those assets over time. Volatility creates urgency; use it to open doors.

Go Deeper

For a deeper dive including how interest rate and market conditions shape strategy selection and how to model scenarios for clients, download our Market Volatility & Estate Planning strategy guide. In the meantime, download the complete cheat sheet for quick reference.

The information provided here does not constitute legal, financial, or tax advice. It is provided for general informational purposes only. This information may not be updated or reflect changes in law. Please consult with an estate attorney, financial advisor, or tax professional who can advise as to your particular situation.

Published: May 01, 2026

Holistic wealth management starts here

Join thousands of advisors who use Vanilla to transform their service offering and accelerate revenue growth.