Jessica Lantz

Jessica Lantz

What’s New in June: A new, reimagined reporting experience, an expanded eMoney integration, and more

Great client conversations are the result of showing up with the right deliverables, the right data, and the right preparation. June’s release addresses all three of these things, with an expanded eMoney integration, on-demand data syncing, and Vanilla’s reporting refresh. We’re especially proud of our new report experience — it’s the most substantial update we’ve ever introduced on that front, and we think it will change how you think about every client deliverable you send.

Confidence at every client conversation

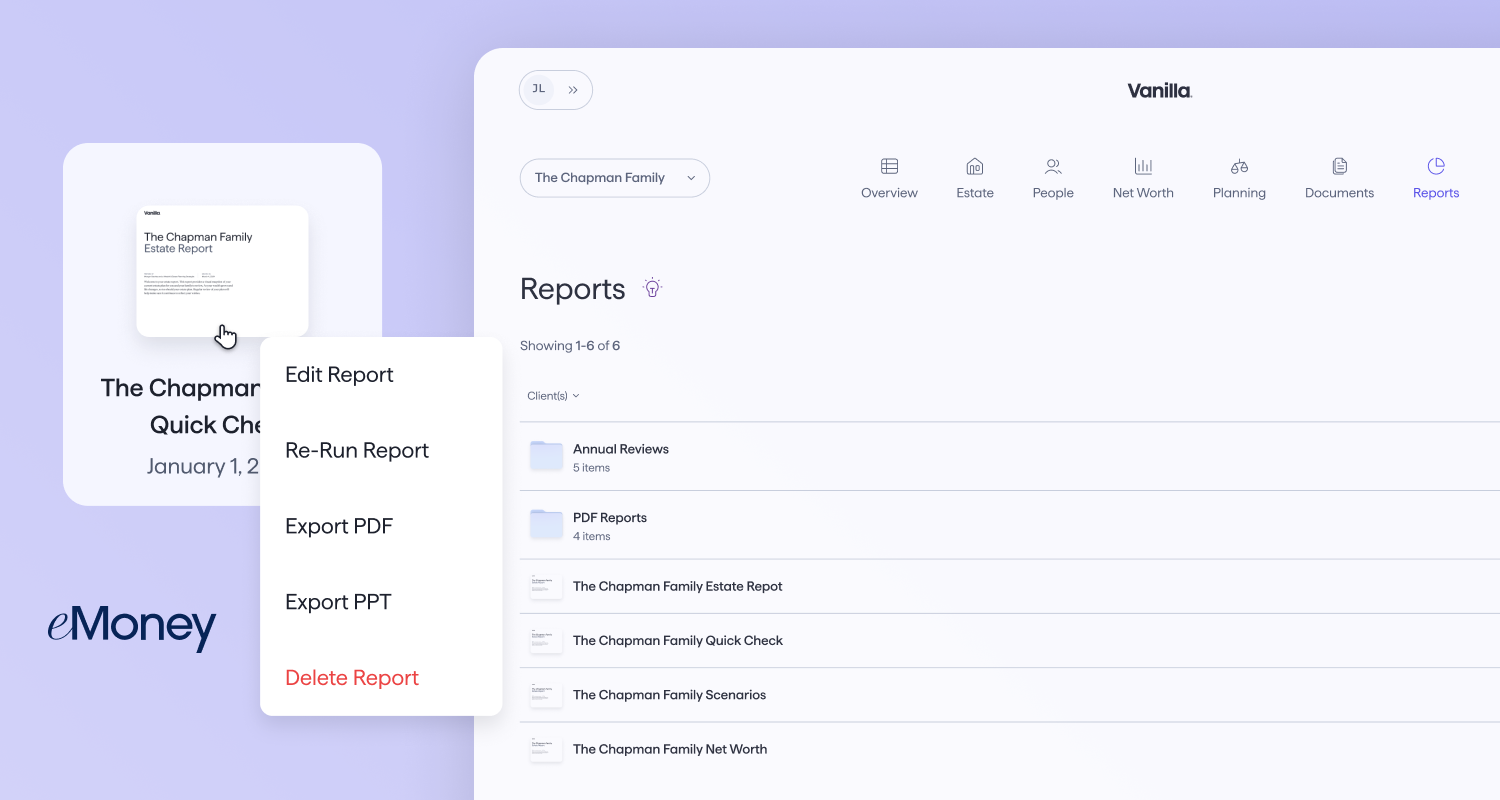

Get to a client-ready report faster — and make it unmistakably yours

The challenge: Client deliverables are often the first thing a client sees from you — and the quality of what lands in front of them should reflect the quality of the planning behind it.

The solution:

- Split-screen editing: Vanilla’s new reporting experience now includes a split-screen editing interface — see your report take shape as you build it, with every change reflected instantly

- Granular controls: Section and slide-level controls let you include exactly what’s relevant for each client, so every page earns its place

- Enhanced customization: Font and color customization options lets report carry your firm’s brand, so the deliverable your client opens feels like it came from you.

- Unified workflow: Download V/AI Summaries and Personal Financial Statements (PFS) directly from the Reports tab

- Saved templates: Capture your strongest report structures and make them the starting point for your whole team

When a report reflects your brand and speaks to your client’s situation, it does more than inform — it demonstrates the standard of care your clients can expect from every interaction. Available now.

Bring a more complete picture of every eMoney client into Vanilla

The challenge: The most productive planning conversations start with a complete client picture — and the faster that picture comes together, the sooner the real work can begin.

The solution:

- New infrastructure: The eMoney integration has been expanded onto a new foundation, delivering a more reliable and capable sync experience

- Beneficiary data: Primary and contingent designations for retirement accounts, annuities, and life insurance now import directly from eMoney, giving your estate profiles visibility into what clients have designated and for whom

- Full account and asset import: A complete range of options now carry over automatically, including bank, investment, real estate, retirement, life insurance, and charitable accounts

- Fractional ownership: Complex ownership structures are reflected accurately from the start, without manual correction

- Override preservation: Edits and overrides made in Vanilla are preserved across syncs, so the work you’ve done building out a client profile stays intact when data refreshes

Advisors who use eMoney as their primary planning tool have more client data at their fingertips than ever — and the more of it that flows into Vanilla automatically, the sooner meaningful planning conversations can begin. Coming soon.

Faster to the moments that matter

Always work with the most current eMoney data

The challenge: Your estate planning advice is only as strong as the data behind it — and you need to trust that what you’re looking at reflects where a client actually stands today.

The solution:

- Automatic sync: Opening a client’s eMoney-connected estate profile now triggers a sync automatically, so you’re always oriented in the most current data from the moment you arrive.

- Manual re-sync: A manual re-sync option gives you control to refresh data on your own terms — so if something changes in eMoney right before a meeting, you can pull it in immediately

- Built-in cooldown: Redundant syncing is prevented across your whole team, so the integration runs smoothly whether one advisor or several are working in the same estate

When the data in your client profile is current before a meeting even starts, every recommendation you make rests on solid ground. Coming soon.

A note on upcoming state estate tax changes

Washington state — effective July 1, 2026

Washington’s estate tax rules are changing July 1st. The two biggest changes your clients will notice:

- The exemption shifts to $3 million (inflation-adjusted annually starting in 2027), and the top marginal rate drops from 35% to 20% — a meaningful difference for larger estates

- The new brackets range from 10% on the first $1 million of taxable estate up to 20% on amounts above $9 million

These new rules are already reflected in Vanilla projections today, with a full switch across the board on July 1.

A few things remain unchanged:

- There is still no portability between spouses of unused Washington estate tax exemption

- The state QTIP election continues to be available

- The ratio approach for nonresident calculations stays the same.

If any of your clients have Washington state exposure, this is a good moment to revisit their plans with the updated numbers in view.

Massachusetts — changes in effect and coming soon

Massachusetts estate tax rules have also changed — and for clients with property both inside and outside the state, the impact on their projections could be significant:

- For Massachusetts residents, out-of-state real estate and out-of-state tangible personal property is excluded from the MA taxable base entirely. Only MA-situated property counts, and any resident whose MA based estate falls below $2 million owes $0 in MA estate tax. This change is retroactive to January 1, 2023 and is reflected in Vanilla today.

- For non-residents who own real estate in Massachusetts, a similar shift is coming soon to Vanilla. Under the updated rule, effective for dates of death on or after August 1, 2025, only the value of MA-situated real estate is taxed for non-residents as well — and the $2 million exemption applies directly to that figure, regardless of total estate size. A non-resident with a $1.5 million MA property and a $13.5 million total taxable estate, for example, would owe $0 in MA estate tax where previously they would have owed over $81,000.

If any of your clients have Massachusetts exposure, now is a good moment to revisit their projections and review the updated rules.

Already a Vanilla customer? Reach out to our CSM team to see these features in action. Exploring Vanilla for the first time? Schedule a demo.

Note that all unpublished features and enhancements mentioned are subject to change in both content and timeline without notice. Vanilla reserves the right to modify or cancel roadmap items at any time.

Published: Jun 30, 2026

Holistic wealth management starts here

Join thousands of advisors who use Vanilla to transform their service offering and accelerate revenue growth.